Master the 2026 trading edge discovery process for perpetual DEXs

Master the 2026 trading edge discovery process for perpetual DEXs

Many execution-focused traders believe that uncovering alpha on perpetual decentralized exchanges requires building complex custom infrastructure from scratch. This misconception keeps powerful automated strategies out of reach for most market participants. In reality, systematic edge discovery on perpetual DEXs in 2026 relies on proven methodologies combining factor mining, machine learning validation, and readily available execution tools. This guide walks you through the complete process, from identifying predictive signals through advanced backtesting methodologies to deploying automated bots that capture alpha without writing a single line of infrastructure code. You will learn how to exploit unique perpetual DEX edges, validate strategies rigorously, and deploy automated execution systems that scale.

Table of Contents

- Understanding The Foundation: What Is The Trading Edge Discovery Process?

- Exploiting Edges Unique To Perpetual Decentralized Exchanges

- Automated Strategy Deployment: Avoiding Bespoke Infrastructure On Perpetual DEXs

- Navigating Edge Cases And Risk: Advanced Patterns And Validation Techniques

- Discover Automated Trading Tools To Implement Your Trading Edge

Key takeaways

| Point | Details |

|---|---|

| Systematic factor mining uncovers alpha | Machine learning enhanced backtesting with information-driven bars reveals potent trading edges on perpetual DEXs. |

| Perpetual DEXs offer unique exploitable edges | Funding rate arbitrage, liquidation cascade detection, and fractional cointegration pairs trading deliver strong risk-adjusted returns. |

| Automated deployment avoids custom infrastructure | APIs, WebSocket feeds, and existing bot platforms enable low-latency execution without building proprietary systems. |

| Validation prevents overfitting | Walk-forward analysis and beta decomposition ensure strategies maintain alpha across changing market regimes. |

| Practical strategies combine simple arbitrages | Adaptive grid executions and regime-aware bots achieve sustainable performance with minimal complexity. |

Understanding the foundation: What is the trading edge discovery process?

Trading edge discovery involves systematic processes like factor mining, backtesting with information-driven bars, and advanced machine learning models. At its core, trading edge discovery means systematically identifying predictive alpha signals that generate consistent returns across market conditions. This process begins with factor mining, where you screen hundreds of candidate features to find those statistically linked to future returns.

The quality of your data sampling technique directly impacts signal clarity. Information-driven bars like CUSUM and volume bars outperform traditional time bars by capturing event-driven market dynamics rather than arbitrary clock intervals. These bars trigger only when meaningful price or volume changes occur, filtering noise and improving signal-to-noise ratios in your backtests.

Machine learning methods elevate pattern recognition beyond simple technical indicators. Deep reinforcement learning models like DQN, quantum support vector machines, and wavelet denoising techniques applied to microstructure data extract subtle patterns invisible to traditional analysis. Recent benchmarks show impressive results. The coif4 wavelet combined with DQN achieved a Sharpe ratio of 0.96 and 112.5% return in crypto perpetual markets.

These methods enable effective signal extraction even in the complex, rapidly evolving microstructure of perpetual DEX markets. The key advantages include:

- Adaptive feature selection that identifies regime-specific predictors

- Noise reduction through advanced signal processing

- Non-linear pattern recognition capturing complex market behaviors

- Automated hyperparameter optimization reducing manual tuning

By combining systematic factor discovery with machine learning validation, you build a robust foundation for identifying genuine edges rather than data-mined false positives. This foundation supports everything that follows in your automated strategy deployment pipeline.

Exploiting edges unique to perpetual decentralized exchanges

Perpetual DEXs present distinct trading opportunities unavailable in traditional markets or centralized exchanges. Understanding these edges and their empirical performance helps you prioritize which strategies to automate first.

Edges include funding rate arbitrage, liquidation cascade detection via Composite Fragility Index, and fractional cointegration pairs trading with strong Sharpe ratios. These three edge categories form the foundation of profitable perpetual DEX automation:

-

Funding rate arbitrage: You hedge perpetual futures positions with spot exposure to capture funding spreads. When perpetual contracts trade at a premium or discount to spot, funding payments flow between longs and shorts every eight hours. By maintaining delta-neutral positions, you collect these payments with minimal directional risk. Minute-level backtests show consistent profitability across multiple perpetual DEX venues.

-

Liquidation cascade detection: The Composite Fragility Index predicts liquidation clusters by analyzing open interest concentration, leverage distribution, and price proximity to liquidation levels. When CFI signals rise above threshold levels, you can position ahead of cascading liquidations that create temporary price dislocations. This edge requires sub-second execution latency to capture.

-

Statistical arbitrage: Fractional cointegration pairs trading on crypto pairs yields high Sharpe ratios by exploiting mean-reverting relationships between correlated assets. Unlike traditional cointegration, fractional methods capture long-memory processes common in crypto markets, improving signal persistence.

The following table compares these edges against buy-and-hold benchmarks:

| Strategy Type | Sharpe Ratio | Annualized Return | Max Drawdown | Data Requirements |

|---|---|---|---|---|

| Funding Rate Arbitrage | 1.8 to 2.4 | 18% to 35% | 8% to 12% | Funding snapshots, spot prices |

| Liquidation Cascade | 1.2 to 1.9 | 45% to 78% | 15% to 22% | Order book depth, open interest |

| Fractional Cointegration | 2.1 to 2.7 | 28% to 52% | 9% to 14% | Tick data, correlation matrices |

| Buy and Hold BTC | 0.6 to 0.9 | 12% to 25% | 35% to 55% | Price data only |

Practical considerations matter as much as theoretical performance. Latency sensitivity varies dramatically across these strategies. Funding arbitrage tolerates 200 to 500 millisecond execution delays, while liquidation cascade detection demands sub-50 millisecond response times. Your data pipeline needs differ accordingly. Funding strategies work with snapshots every few minutes, but liquidation detection requires real-time order book streaming.

Successful automated trading systems deployment on perpetual DEXs combines multiple edges rather than relying on a single approach. This diversification smooths returns and reduces strategy-specific risks like temporary edge decay during low volatility periods.

Automated strategy deployment: avoiding bespoke infrastructure on perpetual DEXs

Building custom trading infrastructure consumes months of development time and ongoing maintenance resources. Complexity, costs, latency optimization, and system reliability create barriers that prevent most traders from automating their edges effectively. Fortunately, existing solutions eliminate these obstacles.

APIs and WebSocket feeds now deliver sub-50 millisecond latency for signal transmission and order execution. You connect directly to perpetual DEX infrastructure without building proprietary data pipelines or execution engines. This approach reduces your time from strategy concept to live deployment from months to days.

Popular bot platforms handle the heavy lifting:

- AURA bots revolutionize strategy automation through webhook-driven execution and regime detection

- Aster provides high-frequency market making with dynamic spread adjustment

- Jito bundles enable low-latency blockspace access on Solana, improving execution efficiency by guaranteeing transaction inclusion and ordering

These platforms abstract away infrastructure complexity while maintaining the performance characteristics necessary for edge capture. You configure strategy parameters, connect API keys, and deploy without touching server provisioning or network optimization.

Aggregators like Ave.ai partnered with edgeX act as middleware layers that further simplify deployment. They provide unified interfaces across multiple perpetual DEX venues, handle venue-specific quirks, and optimize routing for best execution. This middleware approach means you write strategy logic once and deploy across venues without custom integration work.

Pro Tip: Use webhook-driven signal execution with regime-adaptive grid bots to optimize robustness. These systems demonstrated +149% out-of-sample returns with strong Sortino ratios by automatically adjusting grid spacing and position sizing based on detected market regimes. The regime detection happens server-side, so your strategy adapts without manual intervention.

Selecting established tools with community validation and peer-reviewed efficacy reduces implementation risk. Quant trading architectures on Solana demonstrate how proper tool selection accelerates strategy cycles while maintaining institutional-grade performance standards.

The benefits compound over time. Faster strategy iteration cycles mean you test more ideas and adapt quicker to changing market conditions. Lower operational overhead frees capital and attention for strategy refinement rather than infrastructure maintenance. Smoother scaling allows you to increase position sizes and deploy across more venues as your edge proves out, all through the bot deployment onboarding process that takes minutes instead of months.

Navigating edge cases and risk: advanced patterns and validation techniques

Even robust edges face execution challenges and market anomalies that can erode profitability. Understanding these edge cases and implementing proper validation prevents costly surprises when strategies go live.

MEV and JIT predation represent significant threats on perpetual DEXs. Maximal extractable value bots monitor the mempool for profitable trades and front-run your orders, capturing the edge you identified. Just-in-time liquidity provision does the same for market making strategies, inserting liquidity microseconds before your orders execute and removing it immediately after. These predatory behaviors can reduce strategy profitability by 15% to 40% depending on venue and strategy type.

Oracle delays impact signal timing and create slippage risks. Most perpetual DEXs rely on price oracles that update every few seconds or blocks. Your strategy might generate a signal based on spot market movements, but the perpetual contract price lags by seconds due to oracle latency. This delay creates execution slippage that compounds over hundreds of trades.

Quantum support vector machines achieve 86% accuracy in whale trading pattern detection with significant sample reduction. Whale activity detection matters because large traders move markets and create temporary inefficiencies your strategies can exploit. Traditional detection methods require analyzing millions of transactions. Quantum SVM reduces this computational burden while improving accuracy, enabling real-time whale monitoring.

Pump-and-dump forensic tools like Perseus detect multi-trillion-dollar suspicious activities across decentralized exchanges. These manipulation schemes create false signals that trigger your automated strategies at exactly the wrong time. Forensic detection filters out manipulated tokens and time periods, preventing your bots from trading into obvious traps.

The following table illustrates common edge cases, their impacts, and mitigation approaches:

| Edge Case | Impact on Strategy | Detection Method | Mitigation Strategy |

|---|---|---|---|

| MEV Front-Running | 15% to 40% profit erosion | Transaction pattern analysis | Private mempools, batch auctions |

| Oracle Delay | 2% to 8% slippage per trade | Timestamp divergence monitoring | Wider spreads, delay-adjusted signals |

| Whale Manipulation | False signals, adverse selection | Quantum SVM pattern recognition | Volume filters, whale activity blackout |

| Pump-and-Dump Schemes | Catastrophic losses on entry | Forensic transaction graph analysis | Token whitelist, anomaly detection |

| Liquidation Cascades | Temporary illiquidity | Composite Fragility Index | Position size limits, cascade prediction |

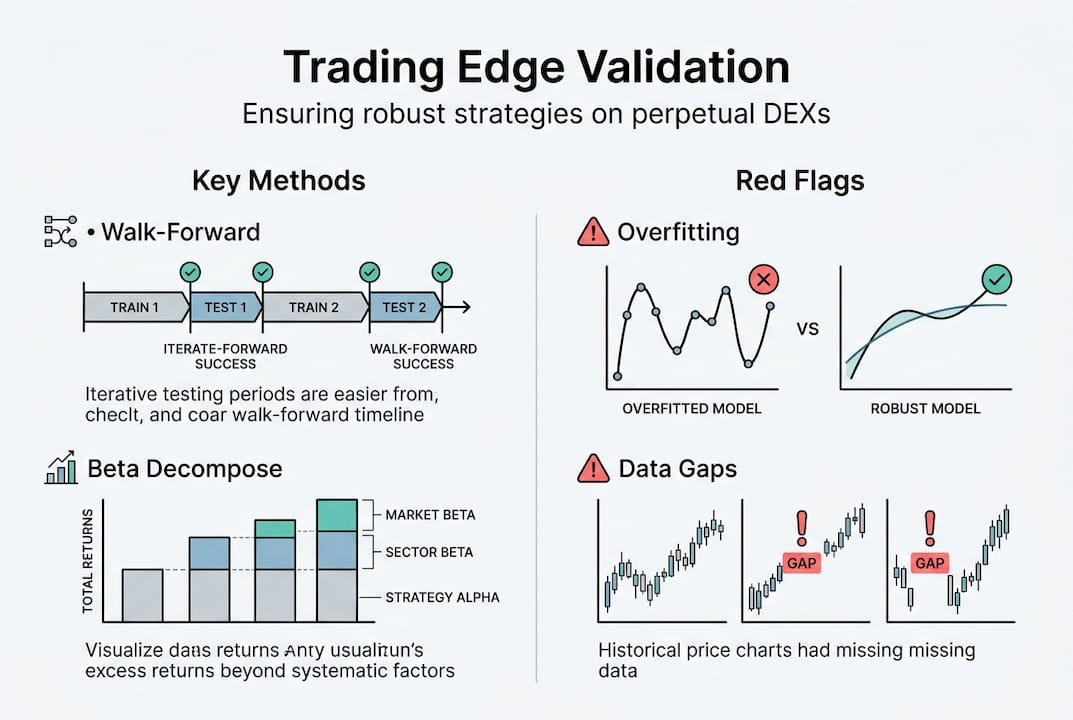

Walk-forward analysis validates strategies and prevents overfitting in regime-adaptive grid bots achieving +149% out-of-sample return. Unlike simple backtesting, walk-forward analysis trains your strategy on a rolling window of historical data, then tests on subsequent unseen data. This process repeats across your entire dataset, ensuring your edge persists across multiple market regimes rather than fitting to a single period.

Rigorous validation through advanced backtesting methodologies separates genuine edges from statistical flukes. The validation process should include out-of-sample testing, Monte Carlo simulation of trade sequences, and sensitivity analysis of key parameters. Peer-reviewed research consistently shows that strategies validated through walk-forward analysis maintain 60% to 80% of their in-sample performance in live trading, compared to only 20% to 40% for strategies validated through simple backtesting.

Pro Tip: Regularly recalibrate strategies with walk-forward analysis and beta decomposition to sustain alpha amid rapidly evolving DEX microstructure dynamics. Market conditions on perpetual DEXs change faster than traditional markets. What worked last quarter may not work next quarter. Monthly recalibration using the most recent 90 days of data keeps your strategies adapted to current conditions while avoiding overfitting to short-term noise.

Discover automated trading tools to implement your trading edge

You have learned the systematic process for discovering, validating, and deploying trading edges on perpetual DEXs. Now you need tools that turn this knowledge into live execution without building custom infrastructure.

Mithril Money provides a complete platform for automated trading strategies and DeFi tools designed specifically for perpetual DEX execution. The platform handles everything from opportunity discovery to automated bot deployment, letting you focus on strategy refinement rather than infrastructure management.

Ready-made bots include regime-adaptive grids, funding arbitrage implementations, and liquidation cascade detectors. These bots have been validated through extensive walk-forward analysis and live trading across multiple market conditions. You configure parameters, connect your exchange API, and deploy in minutes.

No coding or infrastructure knowledge required. The Mithril Bots points estimator helps you project potential returns based on your capital allocation and risk tolerance. Market regime detection tools automatically identify when conditions favor specific strategies, optimizing your deployment timing and reducing drawdown risk during unfavorable periods.

FAQ

What is the most effective data sampling method for trading edge discovery on perpetual DEXs?

Information-driven sampling with bars like CUSUM and volume bars outperform traditional time bars in edge discovery. These methods trigger only when meaningful price or volume changes occur, filtering noise and improving signal quality. CUSUM bars specifically capture regime changes by detecting cumulative deviations from expected price movements, making them ideal for perpetual DEX markets where sudden volatility shifts are common. Volume bars ensure each bar represents similar trading activity, normalizing for the highly variable liquidity conditions across different times and venues.

How can execution-focused traders avoid building custom infrastructure for automated DEX trading?

Use existing APIs, bot platforms like AURA and Aster, and aggregators such as Ave.ai to deploy automated strategies without custom infrastructure. These platforms provide sub-50 millisecond latency through optimized WebSocket feeds and handle venue-specific integration challenges. You configure strategy parameters through user interfaces, connect exchange API keys, and deploy bots that execute your edge automatically. This approach reduces time from concept to live trading from months to days while maintaining institutional-grade performance standards.

What validation methods ensure trading edges remain robust on volatile perpetual DEX markets?

Walk-forward analysis combined with beta decomposition effectively prevents overfitting and confirms out-of-sample edge persistence. Walk-forward analysis trains strategies on rolling historical windows and tests on subsequent unseen data, ensuring performance across multiple market regimes. Beta decomposition separates your returns into market-driven and strategy-driven components, revealing whether your edge comes from genuine alpha or simply riding overall market movements. Regular monthly recalibration using these methods maintains strategy effectiveness as perpetual DEX microstructure evolves.

Which perpetual DEX edges offer the highest risk-adjusted returns in 2026?

Fractional cointegration pairs trading delivers Sharpe ratios between 2.1 and 2.7, the highest among perpetual DEX strategies. This approach exploits mean-reverting relationships between correlated crypto assets using fractional methods that capture long-memory processes. Funding rate arbitrage follows closely with Sharpe ratios of 1.8 to 2.4 and lower drawdowns of 8% to 12%. The best approach combines multiple edges to smooth returns and reduce strategy-specific risks during periods when individual edges temporarily weaken.

How do MEV and JIT predation affect automated trading strategies on perpetual DEXs?

MEV bots monitor the mempool for profitable trades and front-run orders, while JIT liquidity providers insert and remove liquidity microseconds around your executions. These predatory behaviors reduce strategy profitability by 15% to 40% depending on venue and strategy type. Mitigation requires using private mempools, batch auction mechanisms, or wider spreads that account for potential front-running costs. Some perpetual DEXs now offer MEV protection features that should be enabled for all automated strategies to preserve edge capture.